How I Finally Figured Out Variable Income

As a doula, I didn’t have much control over, well, much of anything. Babies come when they want (3 weeks early… 2 weeks late… 3 am…). It was also challenging to figure out finances because although I could say “I’d like 2 clients a month bringing in $XXX please” sometimes I would get sick and miss a birth and have to pay a backup doula. Financially, it was tough!

Variable income is challenging but I am here to tell you that YNAB is the key to making it possible. Here’s how.

Find your “minimum viable income”: what do you absolutely need to make in order to survive a month? Add up the essentials - gas, groceries, housing (rent/mortgage), insurance, etc. By “essentials” I mean “this would rather drastically affect my life if I couldn’t pay this” (ie., they could take my car, shut off electricity, I wouldn’t have anything to eat). For us, Spotify isn’t an “essential” - we could probably survive a month if we couldn’t listen to Cyrille Aimée (though that would be quite sad).

Once you have your “minimum viable income” check it against that minimum amount you would ever expect to make. For many of us, we can reasonably expect to make a certain amount of money. It might not feel like quite “enough”, but do what you can to make sure your minimum income can cover your basics. At the very least, make sure everything that needs to be paid from a checking account can be covered with this money (housing, debt payments, some utilities).

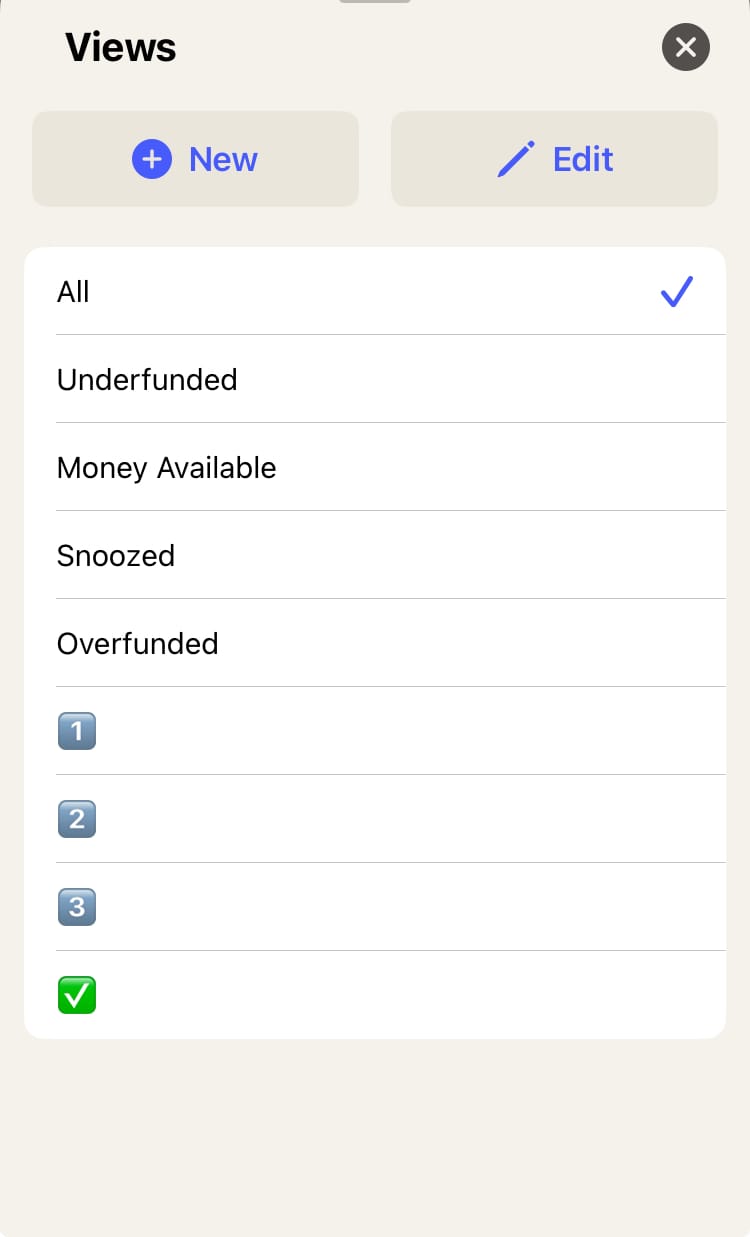

Set up YNAB with a “Priority Waterfall”

Look at your spending plan and set your targets to cover only what you can cover with your “minimum viable income”. It may only be 5-10 categories and that is okay. We have to start somewhere. Next, look at your various expenses and what you want to save for, and mark down the ones that ideally would have more dollars. That might be saving for your next car, some furnishings you would like to have for your home but don’t legitimately need right away, a little extra breathing room in your fun money category, etc. Now write down all the ”I really want these categories to have more money in them each month” on a notepad, index cards, or a google spreadsheet if you’re a nerd like me. We’re going to rank them. Which priority does each category get?

1=essential to fund first

2=I could probably live without it but would really rather not

3=would be nice to have

Now it’s time to really nerd out and set up a focused view on YNAB.

Make a view with #1 priorities, another with #2, and a third with #3.

There will be some months where you have a little extra cash coming in. Perhaps you got a nice little tax refund or some fun money from your husband’s grandma for your birthday. Maybe you worked some overtime and got a sweet paycheck last week. It's possible you found $43 when you (finally) cleaned out your closet.

Each month, make sure to prioritize the essentials - your “minimum viable” expenses - but then after that you get to choose where the money goes! Open up that #1 focus view and put that $43 to good use! Extra fun money! More money for your Emergency Fund! Fully fund your 📚Book category! Oh my!

This will save you from decision fatigue, and it will help you remain flexible so your spending plan can handle life's inevitable curveballs.

While variable income is a bit of a roller coaster, we hope to be able to take away that "stomach leaving your body" feeling every time you see your checking account balance take a bit of a dive. Keep giving every dollar a job, and answering the 5 questions and it will become pretty clear where your money needs to go!

Variable income is tricky. Let me help you get set up so the ups and downs don't make you dizzy anymore.

Schedule your free 30 minute phone consultation to see if we're a good fit!

If you found this helpful, I have a big goal to hit 50 subscribers by the end of the summer. Don't let my dad be my only subscriber! Consider signing up for more witty words of wisdom or sharing this post with a friend.